Pillar Two – Isle of Man Update: What’s on the Horizon?

As the global fiscal landscape continues to evolve, the implementation of Pillar Two of the OECD’s Base Erosion and Profit Shifting (BEPS) framework remains a focal point for governments and corporations alike. The Isle of Man, known for it’s robust financial services sector and commitment to compliance with international tax standards, is in the midst of aligning its tax policies with these notable global reforms. In this update, KPMG delves into the developments surrounding Pillar Two as they pertain to the Isle of man, examining the implications for businesses operating within its jurisdiction. With the potential for changes in corporate tax rates and the introduction of a global minimum tax, stakeholders must stay informed to navigate the complexities ahead. Join us as we explore the latest updates, key actions being taken, and what companies can anticipate in the coming months.

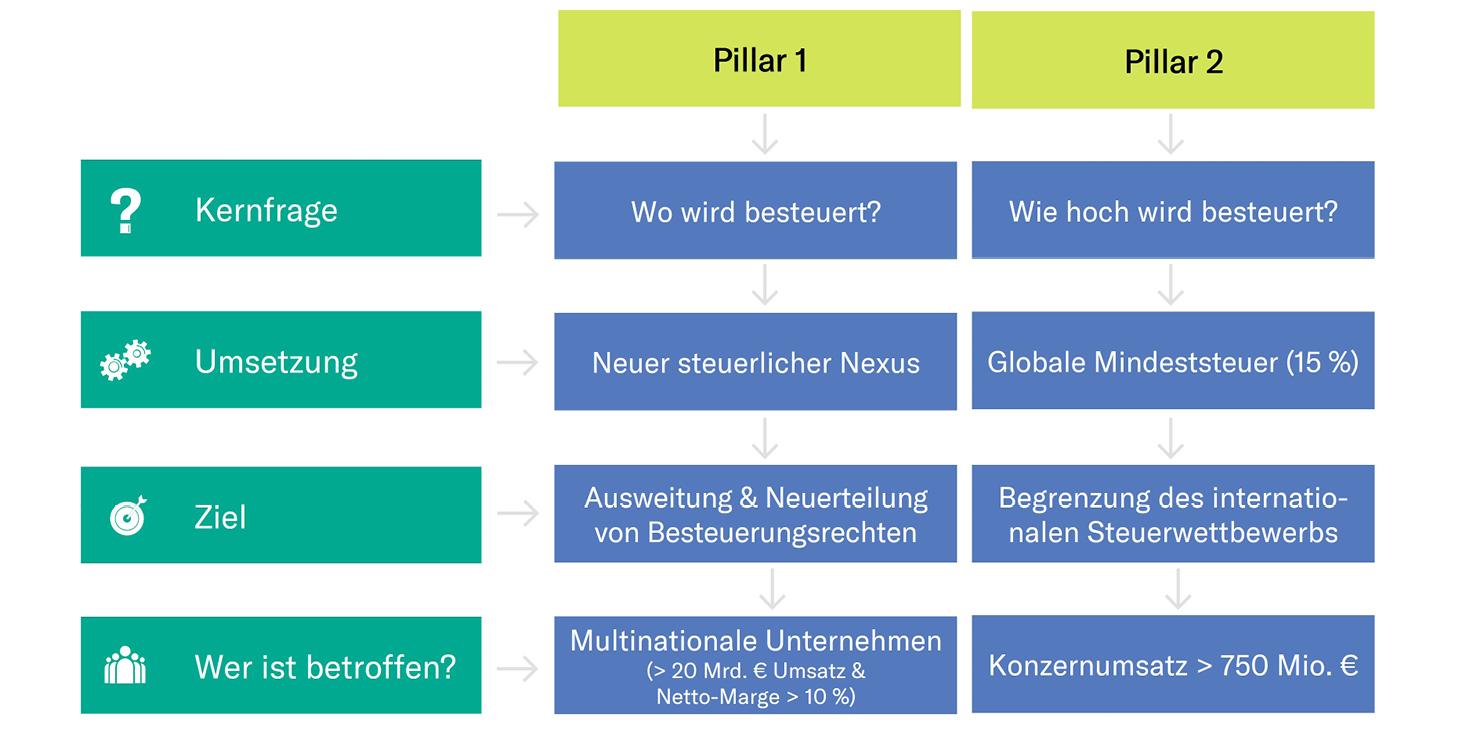

Pillar Two Framework Overview and Its implications for the isle of Man

The implementation of the Pillar Two framework is set to reshape the global tax landscape, providing a minimum tax rate of 15% for large multinational enterprises (MNEs). This initiative aims to address tax avoidance and ensure that profits are taxed where economic activities occur. For the Isle of man, this means adapting its tax strategy to comply with international expectations while maintaining its competitive edge as a business-amiable jurisdiction. Key implications include:

- Reassessment of Tax Policies: The isle of Man will evaluate its existing tax framework to integrate the minimum tax rate,potentially leading to changes in local tax incentives.

- Attractiveness to MNEs: The jurisdiction must balance new regulations with the need to remain appealing to international businesses.

- Compliance and Reporting: Enhanced compliance requirements may necessitate investments in tax governance and reporting mechanisms.

Furthermore,the Pillar Two provisions present both challenges and opportunities for the island. Although the prospect of increased compliance burdens could initially dissuade some businesses, the move toward clarity and fair taxation may enhance the Isle of Man’s reputation on the global stage. Moreover, it provides an opportunity to strengthen relationships with other jurisdictions and foster collaboration.A summary of the potential impacts includes:

| Area | Impact |

|---|---|

| Reputation | Enhancement thru commitment to fair taxation |

| Business Habitat | Potential reevaluation by MNEs |

| Revenue | Impact on tax revenue collection |

Current Developments in the Isle of Mans Adoption of Pillar Two Regulations

The Isle of Man is actively aligning its regulatory framework with the global Pillar Two framework as part of its commitment to ensuring fair tax practices.Recent developments highlight the government’s proactive approach in implementing these regulations,wich aim to establish a global minimum tax rate of 15% for multinational enterprises with significant revenues. Key aspects of this development include:

- Consultative Process: The Isle of Man has engaged in consultations with businesses and stakeholders to gather insights and feedback on the proposed regulations.

- Legislative Updates: Draft legislation is being prepared, with expectations for formal proposals to be presented by the end of the year.

- Alignment with EU Standards: The local government is working to ensure the new regulations are compatible with existing European regulations, fostering cooperation and consistency.

Moreover, the Isle of Man aims to position itself as a competitive jurisdiction while adhering to global tax standards. As part of this endeavor, the island is also considering how revenue thresholds will be defined and the implications for local businesses. the following table summarizes the anticipated timeline for these developments:

| Milestone | Date |

|---|---|

| Public Consultations | Q1 2024 |

| Draft Legislation Release | Q2 2024 |

| Implementation of Regulations | Q1 2025 |

Impact of Pillar Two on Local Businesses and Tax Competitiveness

The implementation of Pillar Two is set to reshape the landscape for local businesses in the Isle of Man, with significant ramifications for tax competitiveness. As multinational corporations adapt to the new global minimum tax regime, smaller enterprises may find themselves in a more challenging environment. Some potential impacts include:

- Increased Compliance Costs: Local companies could face higher administrative burdens as they navigate the complexities of the new tax framework.

- Competitive Pricing Pressure: With larger firms potentially adjusting their tax strategies, smaller businesses may struggle to offer competitive pricing.

- Investment Attraction: The Isle of Man might need to reassess its tax incentives to continue attracting foreign investment and retain local startups.

Furthermore,while the goal of Pillar Two is to establish a fairer tax system globally,its execution could inadvertently disadvantage local firms not equipped to handle these changes. As businesses recalibrate, the focus will be on:

- Innovation and Adaptation: Local firms will need to leverage innovation to remain relevant in a shifting marketplace.

- collaborative Strategies: Partnerships may become vital for smaller companies to maximize resources and navigate the new tax landscape.

- Advocacy for Policy Adjustments: Engaging with policymakers will be essential to ensure that the unique needs of local businesses are considered.

| Impact Area | Potential Influence |

|---|---|

| Compliance Costs | Increased operational expenses |

| Market Dynamics | Pressure on pricing strategies |

| Investment Climate | Re-evaluation of tax incentives |

Recommendations for Compliance and Strategic Planning for Isle of Man Entities

As Isle of Man entities navigate the implementation of the Pillar Two framework,ensuring compliance while maintaining strategic agility is crucial. Organizations should focus on enhancing their governance structures to ensure that they meet both local and international tax obligations effectively. Key recommendations include:

- Regular Compliance Audits: Conduct internal audits to assess compliance with new regulations and identify any potential gaps.

- Stakeholder Engagement: Foster dialog with stakeholders, including tax authorities and industry peers, to stay informed on evolving compliance standards.

- Data Management Oversight: Invest in robust data collection and analysis systems to ensure accurate reporting and transparency.

- Training and Development: Provide continuous education for staff on compliance requirements and strategic planning to adapt to changing regulations.

Additionally, strategic planning should incorporate a proactive approach to risk management in the face of global tax reforms. Entities are advised to consider the following strategies:

- Diversification of Tax Strategies: Evaluate and adjust tax strategies to align with both domestic and international expectations, minimizing the risk of double taxation.

- Scenario Planning: Develop multiple financial models to anticipate various outcomes from changes in international tax policies.

- Collaboration with Advisors: Engage with tax and legal advisors to navigate complexities and optimize compliance efforts.

Future Outlook: Navigating the Global Tax Landscape Post-Pillar Two Implementation

The implementation of Pillar Two represents a significant shift in the global tax paradigm, compelling jurisdictions, including the Isle of Man, to recalibrate their tax strategies to ensure compliance and attract foreign investments.As nations move towards a minimum tax framework,it becomes essential for entities operating within the Isle of Man to prepare for adjustments in corporate tax liabilities. Businesses must consider a range of implications, including:

- Increased compliance Requirements: Companies may face heightened reporting obligations as they align with new international standards.

- Strategic Tax Planning: Firms should reassess their tax structures and operational models to optimize tax efficiencies while complying with international guidelines.

- Potential Competitive Disadvantages: As the global playing field evolves, organizations may experience shifts in competitive dynamics, necessitating agile responses.

In this context, a proactive approach to the changing fiscal environment is pivotal. The Isle of Man’s administration and businesses must engage collaboratively to navigate these challenges effectively. To foster this adaptability, stakeholders could consider the following measures:

| Measure | Description |

|---|---|

| Continuous Monitoring | Implement systems to track changes in global tax regulations and their implications. |

| Stakeholder Collaboration | Facilitate ongoing dialogue between government, tax advisors, and businesses to ensure aligned strategies. |

| Education & Training | Invest in training programs to equip teams with knowlege on compliance and strategic tax management. |

Wrapping Up

the developments surrounding Pillar Two on the Isle of Man mark a significant step in aligning global tax frameworks with the evolving demands of multinational corporations. The recent update from KPMG highlights the island’s commitment to maintaining its competitive edge while embracing transparency and cooperation in the international tax landscape.As the Isle of Man navigates these changes, stakeholders must remain vigilant and informed. The implications of Pillar Two will undoubtedly reverberate across jurisdictions, influencing corporate strategies, compliance obligations, and the broader economic environment. Moving forward,continuous engagement with regulatory updates and the evolving interpretations of these measures will be essential for businesses aiming to thrive amidst this transformative era in global taxation.